🎧 Morning Brief #117 - audio debate on today’s market setup

Two independent indicators are simultaneously describing the same reality: holding Bitcoin right now means accepting risk without adequate compensation. The Bitcoin Risk Meter has moved deep into negative Sharpe territory, and the MVRV Z-Score has dropped below its 365-day moving average - both signals suggest the market is not ready for a sustained recovery.

TL;DR

The Sharpe Ratio is in deeply negative territory (-63 on the 365d, -287 on the fast version), and the MVRV Z-Score is at 0.49 - below its historical mean. The market is not paying for risk: risk-adjusted returns are negative, and network valuation is neutral but does not provide a buy signal.

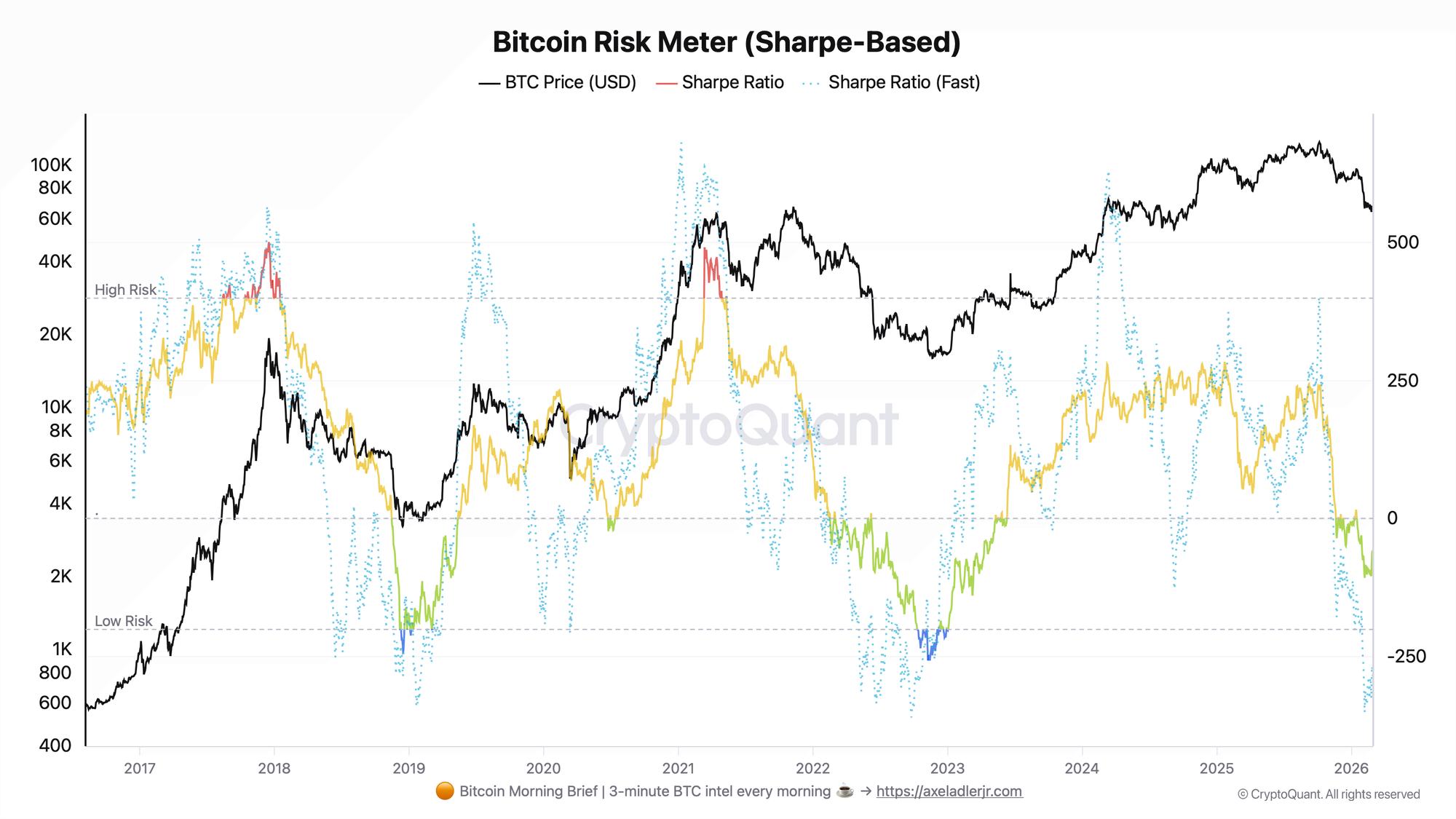

Bitcoin Risk Meter (Sharpe-Based)

The metric is built on the 365-day rolling Sharpe Ratio and its fast version (180 days). Positive values mean the market compensates volatility with returns. Negative values mean it does not.

As of March 1, 2026, the Sharpe Ratio (365d) stands at -63, and the fast version (180d) at -287. The metric is scaled for visualization and used as a relative regime indicator rather than a classic Sharpe in absolute terms. This means: over the past six months to one year, Bitcoin has generated negative risk-adjusted returns - volatility was not compensated by performance. The move into negative territory began in January 2026 and accelerated in February under price pressure. For context: the cycle low of this indicator in 2022 was recorded at -257 on the Sharpe (365d) - current values on the fast version are already approaching that zone, while the slow indicator remains well above the bottom.

As long as the Sharpe (365d) stays negative, the market is officially "not paying for risk." This is not a sell signal in itself, but it is a strong argument against adding to positions. The reversal trigger would be a sustained recovery of Sharpe Fast above -100 alongside price stabilization.

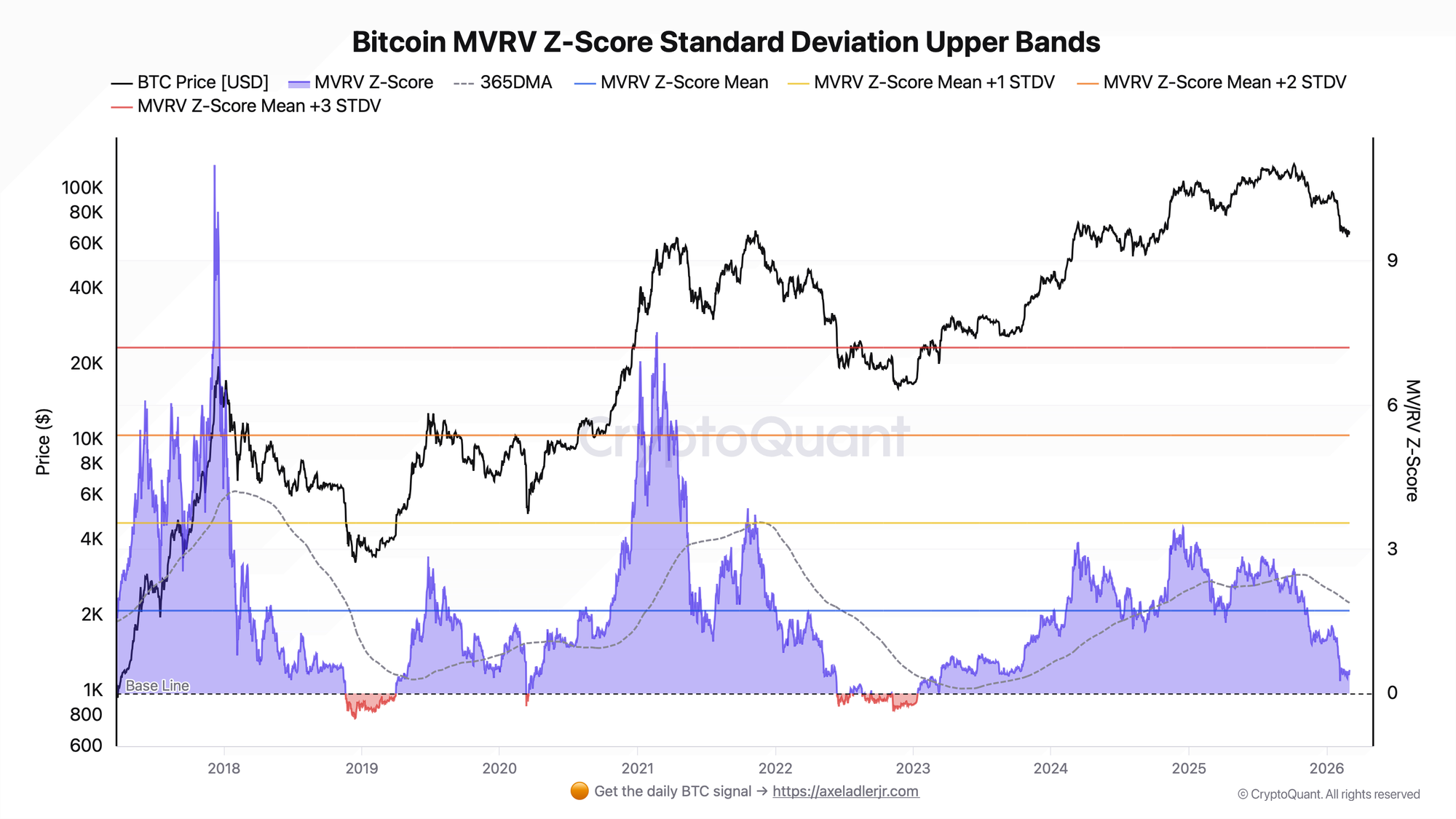

Bitcoin MVRV Z-Score Standard Deviation Upper Bands

The MVRV Z-Score compares market capitalization to realized capitalization; values above +1 STDV (~3.55) signal overheating, values near the zero line indicate neutral valuation, and negative values (red zone, Base Line) mark historical capitulation events when market price fell below the average holder's cost basis.

As of March 2, 2026, the MVRV Z-Score is 0.49 - below the 365-day moving average (1.89) and below the historical mean (1.73). This is a neutral valuation zone: the network is not overheated, but it has not capitulated either. The distinction matters: historically, strong buy signals from MVRV appeared when the Z-Score moved into negative territory (red zone on the chart - 2019, 2020, 2023), not simply when it declined to 0.5. The current level only indicates the absence of an unrealized profit overhang - that is not sufficient for a reversal signal.

The absence of overheating protects against a sharp collapse but does not create conditions for buying. A bullish signal from MVRV would require either a move into negative territory (historical capitulation levels) or a recovery above the 365DMA (1.89) accompanied by a trend shift in price.

Connection. Both indicators point to the same phase but from different angles: Sharpe says "returns do not justify the risk," MVRV says "valuation is neutral but not cheap by historical capitulation standards." This is neither a bearish extreme nor a bullish signal - it is a zone of uncertainty where the market requires an additional catalyst to shift the regime in either direction.

😟 Stop holding through every crash - start your 7-day free trial. Weekly Engine tells you when to stay in, when to step aside, and when risk is rising.

FAQ

Is "Low Risk" on the chart a buy signal? No, and this is an important terminological distinction. "Low Risk" in the context of this metric means the Sharpe Ratio is negative - that is, the market is in a phase of low or negative risk-adjusted returns. Historically, growth resumed after exiting such zones, but entering the zone itself is a signal for caution, not for buying.

Under what conditions would a real reversal signal appear? For MVRV - either the Z-Score moves into negative territory (red Base Line area) or recovers above 1.89 (365DMA) with price confirmation. For Sharpe - a sustained recovery of the fast version above -100 followed by a zero-line crossover. Alignment of both conditions is a strong argument for a positioning change.

CONCLUSIONS

The Bitcoin Risk Meter and MVRV Z-Score are simultaneously in zones that provide neither a buy signal nor a signal for aggressive selling. Sharpe (365d) at -63 indicates the market is not compensating for the risk taken - that is an argument against adding to positions. MVRV Z-Score at 0.49 removes the unrealized profit overhang, but historical capitulation zones (negative values) remain far away - the metric is not giving a "everything has crashed, time to buy" signal.

Current regime: a transitional phase with negative risk-adjusted returns and neutral network valuation - the market is waiting for a catalyst to shift the regime. The primary trigger for a shift to a bullish regime is either MVRV Z-Score moving into negative territory or recovering above 1.89 alongside a Sharpe recovery. The primary risk is that the macro environment keeps Sharpe negative longer than historical analogs would suggest, prolonging the phase of uncertainty.