Discover how Global M2 and Spot ETF netflows are overriding the traditional Bitcoin halving cycle. Learn the thresholds, SQL formulas, and how to trade them.

TL;DR

- What it is: A macro-valuation framework that measures fiat liquidity (Global M2 YoY) and structural demand (Spot ETF Netflows) against Bitcoin's fixed supply schedule.

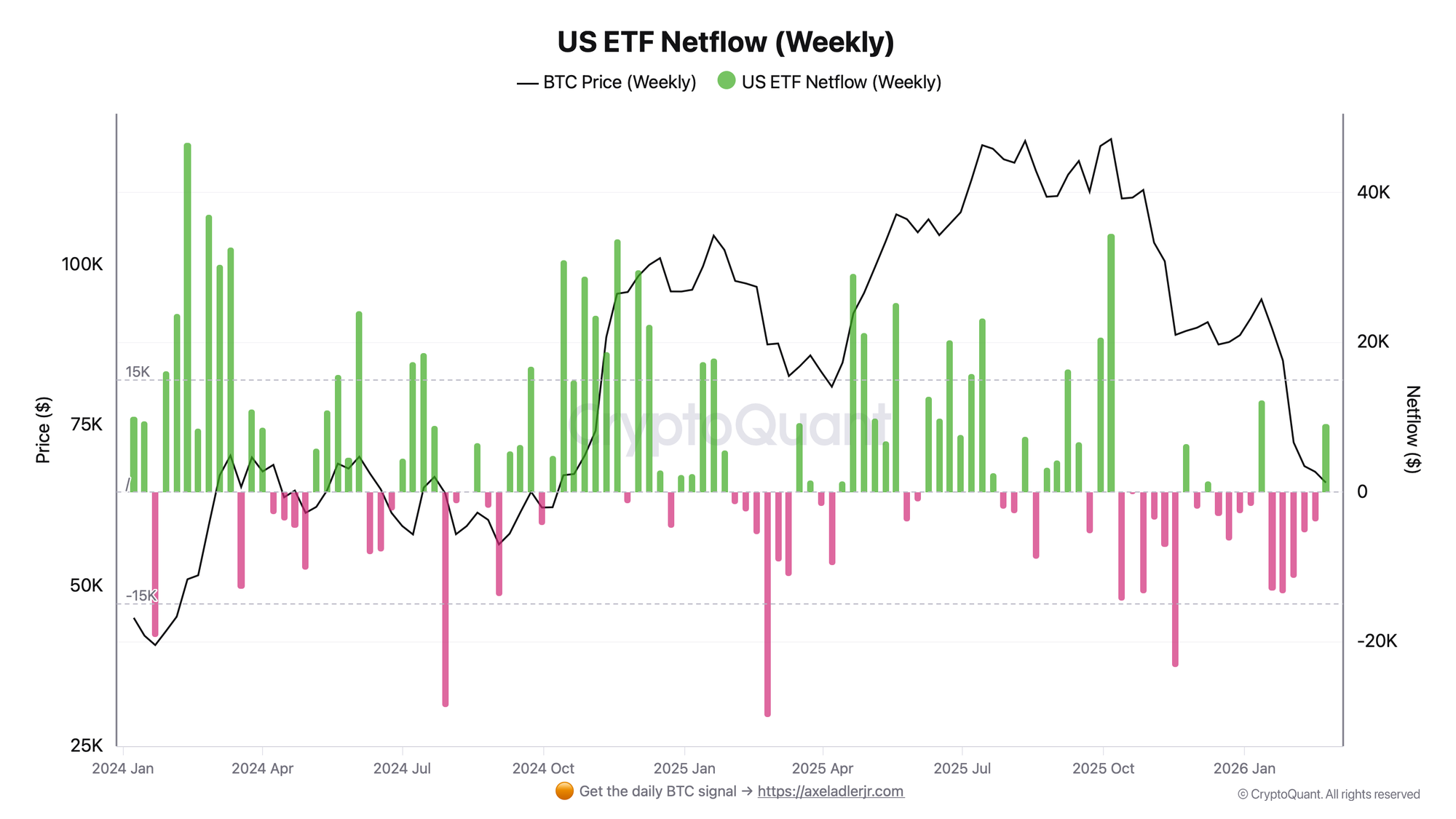

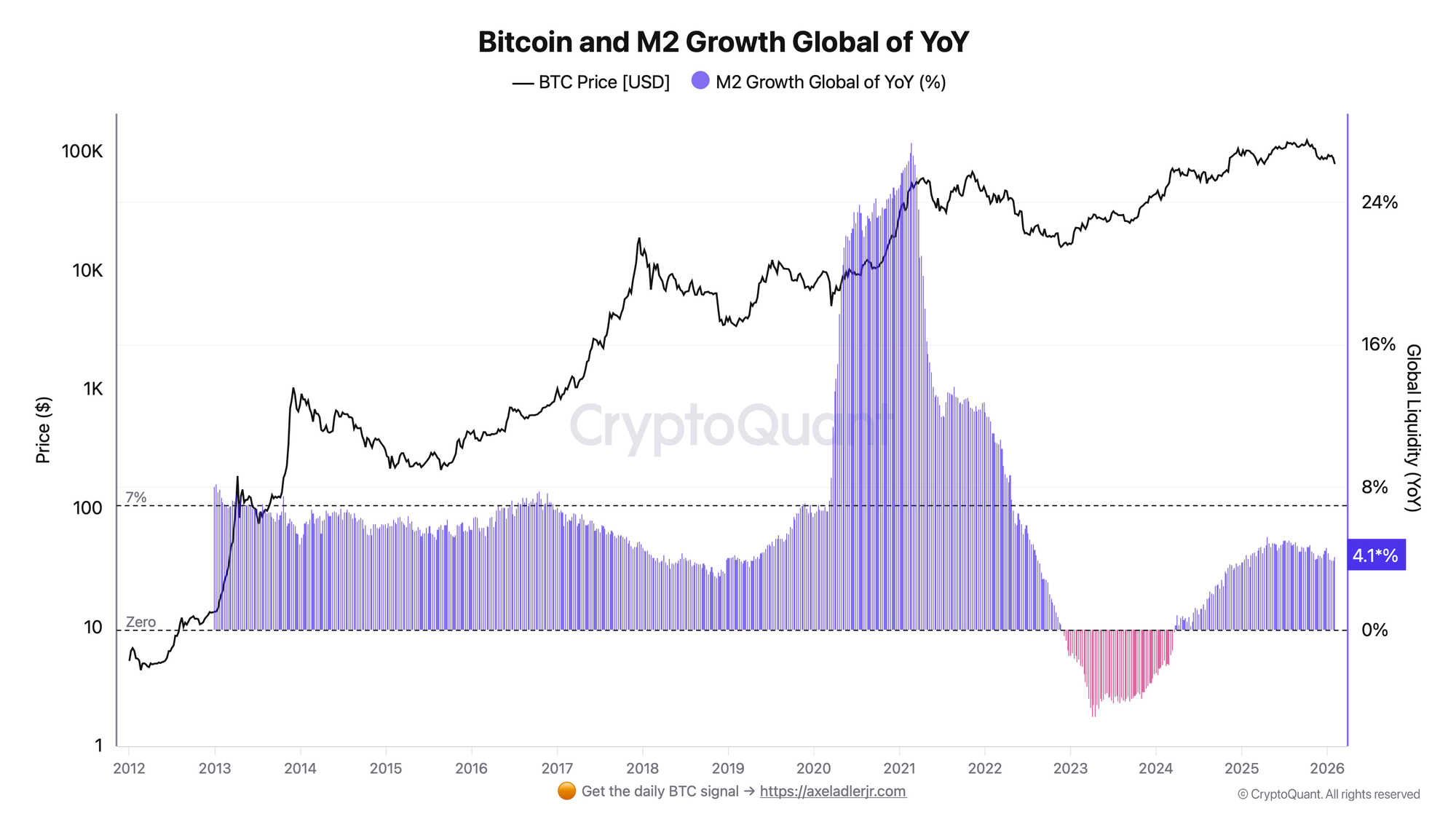

- How it’s calculated: We measure the Year-over-Year (YoY) percentage change in Global M2 money supply, combined with the 7-day rolling sum of US Spot ETF net inflows.

- What "Up/Down" means: Expanding M2 + positive ETF inflows = bullish (cycle acceleration). Contracting M2 + negative ETF outflows = bearish (cycle suppression).

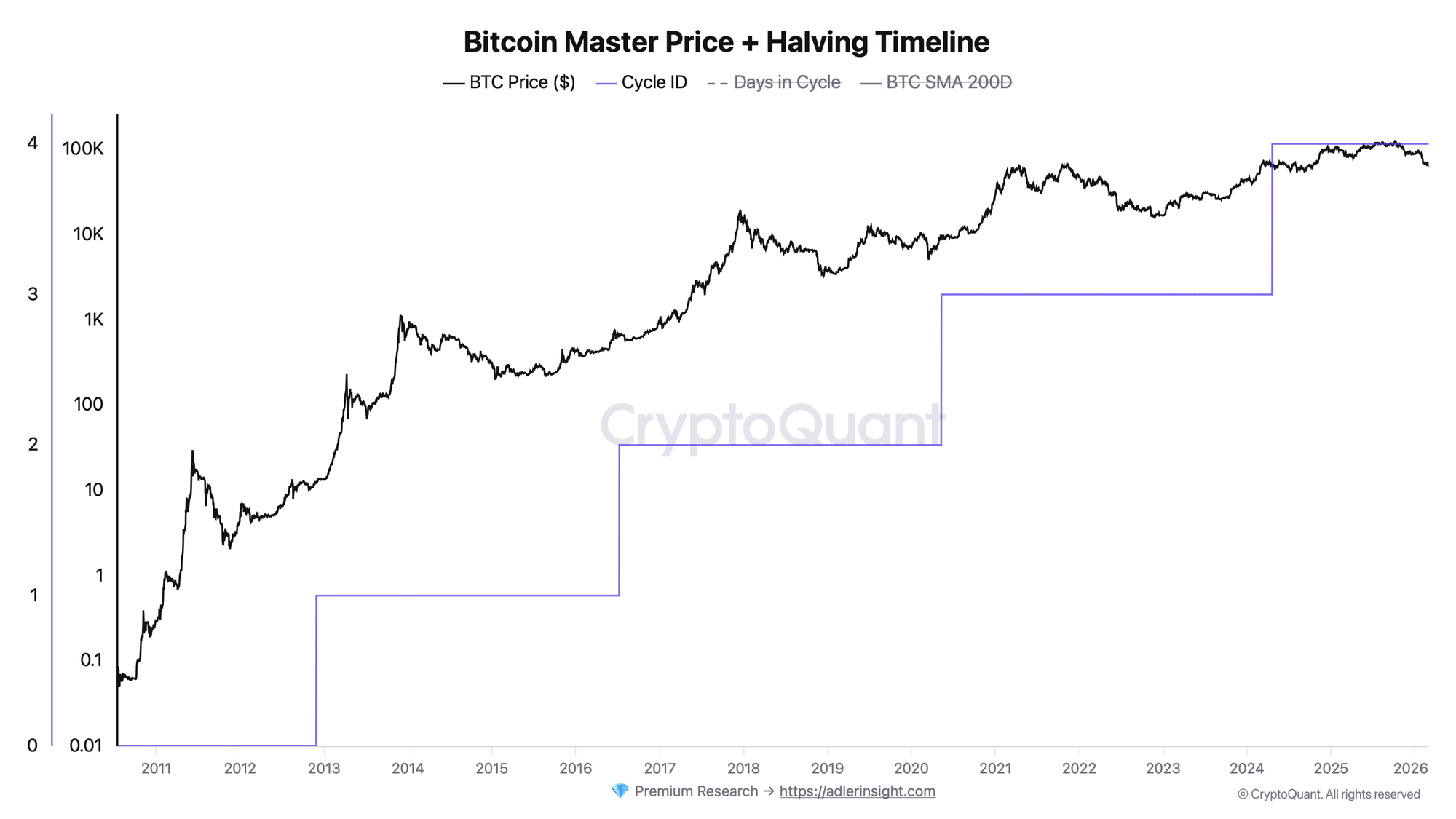

- Core practical takeaway: Macro liquidity and ETF inflows now dictate cycle timing and drawdowns more than the 210,000-block halving schedule.

- Context/false signals: ETF inflow reports can lag actual price movements; buying purely on backward-looking ETF prints during extreme greed (for example, MVRV > 5) is a trap.

- The mini-rule: Signal triggers bullish when Global M2 YoY flips from negative to positive AND weekly US ETF netflows sustain > 5,000 BTC for two consecutive weeks.

The signal rule

Formula:

Cycle Strength = (Global M2 YoY Growth > 0%) + (Weekly ETF Netflow > 0)

Thresholds and window:

- Bullish: M2 YoY > 2.0% AND Weekly ETF netflows > 10,000 BTC. This indicates strong fiat liquidity expansion combined with direct institutional buying.

- Bearish: M2 YoY < 0% (contraction) AND Weekly ETF netflows < -2,000 BTC. The halving supply shock will not save the price in this environment.

- Neutral: M2 is flat (0% to 1%), and ETF flows are mixed. The market reverts to standard

days_into_cycleand miner dynamics.

Examples:

- If M2 YoY turns negative (as it did during the 2022 tightening cycle), then the market can remain in a severe bear phase regardless of where we are in the 4-year cycle.

- If spot ETF demand absorbs a large share of net new supply for multiple weeks, then cycle timing can shift forward (including pre-halving highs), breaking the historical pattern.

SQL / Code snippet

Calculates weekly Global M2 YoY growth against weekly Bitcoin price (BigQuery-compatible). This version actually aggregates to weekly data so the YoY LAG(52) is consistent.

-- Weekly (Sunday) aggregation + YoY change (52 weeks)

WITH price_daily AS (

SELECT

DATE(datetime) AS day,

c AS price

FROM `tech-web3-analytics-prod.abstraction_price.btc_usd_index-price_day`

WHERE DATE(datetime) >= '2012-01-01'

),

m2_daily AS (

SELECT

DATE(event_timestamp) AS day,

AVG(value) AS m2_value

FROM `poc_stage.tradfi_fred_dataset`

WHERE type = 'm2' AND DATE(event_timestamp) >= '2012-01-01'

GROUP BY 1

),

price_weekly AS (

SELECT

DATE_TRUNC(day, WEEK(SUNDAY)) AS week,

AVG(price) AS price

FROM price_daily

GROUP BY 1

),

m2_weekly AS (

SELECT

DATE_TRUNC(day, WEEK(SUNDAY)) AS week,

AVG(m2_value) AS m2_value

FROM m2_daily

GROUP BY 1

)

SELECT

w.week,

p.price,

100 * SAFE_DIVIDE(p.price - LAG(p.price, 52) OVER (ORDER BY w.week),

LAG(p.price, 52) OVER (ORDER BY w.week)) AS price_yoy,

100 * SAFE_DIVIDE(m.m2_value - LAG(m.m2_value, 52) OVER (ORDER BY w.week),

LAG(m.m2_value, 52) OVER (ORDER BY w.week)) AS m2_yoy

FROM (SELECT week FROM m2_weekly UNION DISTINCT SELECT week FROM price_weekly) w

LEFT JOIN price_weekly p USING (week)

LEFT JOIN m2_weekly m USING (week)

ORDER BY 1 DESC;

Key definitions

- Global M2 YoY: The year-over-year percentage change in the total supply of currency and highly liquid assets circulating in the global economy.

- Spot ETF netflow: The absolute daily or weekly difference between capital entering and leaving US-listed spot Bitcoin ETFs.

- Halving block subsidy: The deterministic reduction in new Bitcoin issuance (currently 3.125 BTC per block), which has historically anchored the 4-year cycle.

How to interpret this metric

- Bullish case: When Global M2 YoY growth is accelerating and spot ETF flows show sustained weekly net-positive inflows. In this regime, fiat liquidity pushes capital into risk assets, and ETFs act as a direct structural vacuum for Bitcoin's fixed supply. Expect cycle highs to stretch higher or occur earlier than the traditional day-500 timeline.

- Bearish case: M2 YoY turns negative (central bank tightening) accompanied by ETF net-outflows. Liquidity is draining from the system. In this state, the mechanical reduction of miner supply (halving) can be overpowered by macro sell pressure.

- Neutral case: M2 growth is stagnant and ETF flows chop between positive and negative. The market is waiting for a macro catalyst.

- What matters most: The macro trend of M2 (months) combined with cumulative ETF flow (weeks), rather than a single day of ETF outflows.

Historical examples (what worked, what didn’t)

- Q1 2024 (the pre-halving ATH):

- Indicator: Spot Bitcoin ETFs saw net inflows of roughly $12B in Q1 2024.

- Result: Bitcoin hit an all-time high before the halving event for the first time in history.

- Context: Structural demand routed through ETFs compressed cycle timing and overpowered the standard early-cycle accumulation narrative.

- Indicator: Spot Bitcoin ETFs saw net inflows of roughly $12B in Q1 2024.

- Late 2022 (macro overload):

- Indicator: Broad money growth rolled over during the 2022 tightening cycle and liquidity conditions deteriorated sharply.

- Result: Bitcoin reached the deep bear market low around ~$15,900.

- Context: Even deep into the historical cycle window, liquidity drawdowns can dominate the halving schedule.

- Indicator: Broad money growth rolled over during the 2022 tightening cycle and liquidity conditions deteriorated sharply.

How to use it in practice

- Setup: You track

days_into_cycle(for example, nearing the historical day-500 top zone) but want to know if liquidity will extend or cut the cycle short. - Trigger: Global M2 YoY crosses above 4% AND weekly ETF netflows remain positive for 3 consecutive weeks.

- Confirm: Confirm with the MVRV Z-Score (remaining below 5.0 suggests room without overheating) and STH SOPR (bouncing off 1.0).

- Invalidates when: Liquidity conditions tighten materially (for example, M2 re-accelerates downward) or consecutive ETF outflow weeks exceed -10,000 BTC total.

- Action: Scale into positions when M2 flips positive; begin taking profit if M2 growth stalls and ETF flows turn negative for a multi-week period, regardless of what "cycle day" it is.

Common pitfalls

- Ignoring the ETF settlement/reporting lag: ETF flow data is typically reported end-of-day. Trading purely on yesterday's flow means you are reacting to priced-in data. Filter: use ETF flows for weekly trend strength, not intraday entries.

- Confusing nominal M2 with YoY M2: The absolute number of M2 always looks large. Filter: the YoY rate of change (acceleration/deceleration) is what matters for macro regimes.

- Assuming ETFs only buy: In a macro downturn, ETFs can become a source of liquid supply. Filter: watch for consecutive outflow weeks during M2 contraction to identify regime shifts early.

Halving supply shock vs fiat liquidity

- Halving supply: Reduces issuance mechanically (for example, ~900 BTC/day to ~450 BTC/day). Predictable, but impact diminishes as market cap grows.

- Fiat liquidity (M2/ETF): Introduces large, variable demand shocks (for example, ETFs absorbing multiples of net new issuance in strong weeks). Less predictable but can carry more marginal price impact than the halving.

FAQ

- Q: Does the 4-year cycle still work after spot ETFs?

- A: The cycle phases (accumulation, bull, distribution, bear) remain, but timing and magnitude are now more sensitive to ETF flows and macro liquidity.

- A: The cycle phases (accumulation, bull, distribution, bear) remain, but timing and magnitude are now more sensitive to ETF flows and macro liquidity.

- Q: Where can I find Global M2 data?

- A: You can source it from aggregated central bank datasets, or construct a proxy index from major regions. (FRED is useful for US series; global requires aggregation.)

- A: You can source it from aggregated central bank datasets, or construct a proxy index from major regions. (FRED is useful for US series; global requires aggregation.)

- Q: What is a significant weekly ETF netflow value?

- A: As a practical rule, consecutive weeks of > 5,000 BTC net inflows imply strong demand, while consecutive outflows below -2,000 BTC can signal distribution.

- A: As a practical rule, consecutive weeks of > 5,000 BTC net inflows imply strong demand, while consecutive outflows below -2,000 BTC can signal distribution.

- Q: Why did Bitcoin drop in 2022 when the cycle should have bottomed?

- A: Liquidity conditions tightened aggressively during 2022, overpowering the historical cycle timing.

- A: Liquidity conditions tightened aggressively during 2022, overpowering the historical cycle timing.

Related guides

- Overview: The 4-Year Bitcoin Cycle: Definition, Mechanics & Historical Evidence

- Confirmations: MVRV Z-Score: How to Identify Bitcoin Market Tops and Bottoms

- Confirmations: Bitcoin STH SOPR: What It Is and How to Use It

- Capitulation triggers: Bitcoin Hash Ribbons: Capitulation Signals & Buy Triggers

- Miner data: Bitcoin Puell Multiple: Definition, Formula & Miner Signals

Minimal conclusion

- Global M2 YoY is the macro engine; spot ETFs are the transmission mechanism into Bitcoin.

- The 4-year cycle sets a baseline schedule, but M2 and ETFs can dictate actual highs and lows.

- Do not trade the halving schedule blindly without checking current liquidity regimes.

- Next step: Learn how to time macro tops by combining ETF flows with MVRV Z-Score: How to Identify Bitcoin Market Tops and Bottoms.